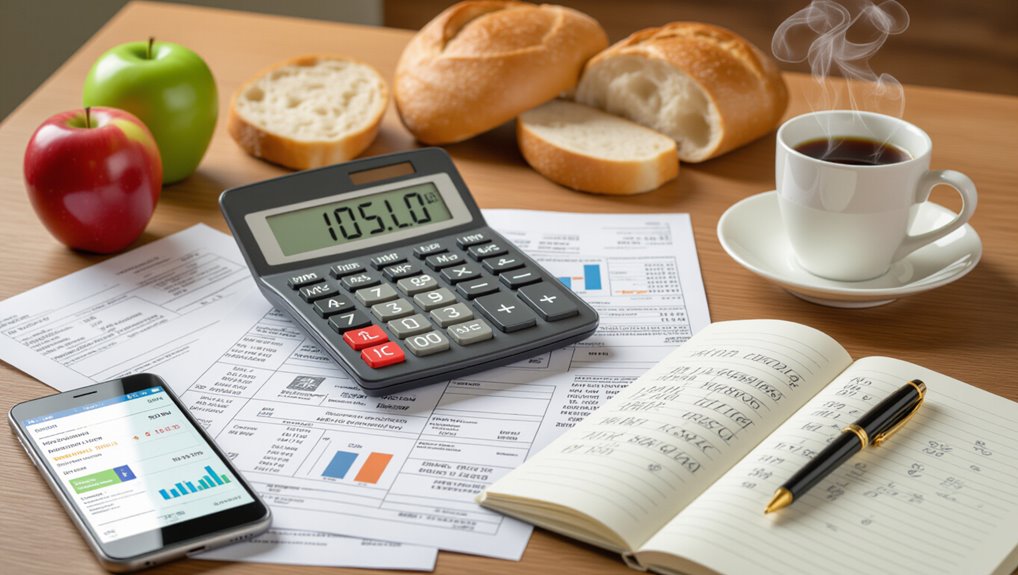

Calculating the inflation rate is surprisingly simple once you understand the basic formula. First, find the Consumer Price Index (CPI) for two different time periods you want to compare. Then use this formula: subtract the old CPI from the new CPI, divide by the old CPI, and multiply by 100. For example, if CPI rises from 105 to 110, the calculation is (110-105)/105 x 100, which equals 4.8% inflation. This step-by-step process helps anyone track how much more expensive things have become over time.

Understanding inflation can feel like trying to hit a moving target, but calculating the inflation rate is actually more straightforward than many people think. At its core, inflation measures how much more expensive things become over time. Think of it like tracking whether your favorite pizza costs more this year than last year.

The process starts with creating a basket of goods and services that represents what average consumers buy. This basket includes everyday items like food, housing, gas, and healthcare. Government agencies like the Bureau of Labor Statistics update this basket regularly based on spending surveys, ensuring it reflects real shopping habits rather than outdated patterns.

Next comes the data collection phase. Workers visit stores and check online prices for every item in the basket. They do this monthly or quarterly, creating a thorough picture of current costs. It’s like having thousands of comparison shoppers working together to track price changes across the entire economy.

These prices get turned into something called the Consumer Price Index, or CPI. The calculation compares today’s basket cost to a base year, which is set at 100 for easy reference. The formula is simple: divide the current basket cost by the base year cost, then multiply by 100. If your basket costs $105 today and cost $100 in the base year, your CPI is 105.

The actual inflation rate comes from comparing two time periods using this formula: subtract the old CPI from the new CPI, divide by the old CPI, then multiply by 100. For example, if the CPI goes from 100 to 105, the inflation rate is 5 percent.

Here’s a practical example: if last year’s CPI was 105 and this year’s is 110, the calculation looks like this: 110 minus 105 equals 5, divided by 105 equals 0.048, multiplied by 100 equals 4.8 percent inflation. This exponential growth means that higher prices from one year become the foundation for calculating the next year’s inflation impact.

Economists sometimes adjust these numbers by removing volatile items like gas and food prices to see clearer trends. This helps policymakers understand whether price changes represent temporary spikes or lasting economic shifts. These calculations are crucial because they influence monetary policy decisions and help central banks determine whether to adjust interest rates to maintain economic stability. Understanding these inflation measurements is particularly important for investors, as rising prices can significantly erode the purchasing power of their portfolios over time.

Frequently Asked Questions

What Is the Difference Between Headline Inflation and Core Inflation?

Headline inflation measures price changes for everything consumers buy, including groceries and gas.

Core inflation excludes food and energy prices because they jump around like a bouncing ball due to weather or world events.

Think of headline inflation as the full shopping cart, while core inflation removes the most unpredictable items.

Policymakers prefer core inflation since it shows steadier, long-term trends without temporary price spikes.

How Often Is the Consumer Price Index Updated and Released?

The Consumer Price Index gets updated and released monthly by the Bureau of Labor Statistics.

Each release happens around the second or third week of the month at 8:30 AM Eastern Time. The data covers the previous month’s prices – so November’s release shows October’s inflation numbers.

Occasionally releases get rescheduled for holidays or government closures, but this rarely happens.

Can Inflation Rates Be Negative, and What Does That Mean?

Yes, inflation rates can turn negative, which economists call deflation. This means prices for goods and services actually decrease over time.

While cheaper groceries might sound appealing, deflation creates serious economic problems. It makes debts harder to repay and can lead businesses to cut jobs.

Countries like Japan experienced prolonged deflation, causing economic stagnation that lasted years.

Which Countries Have Experienced the Highest Inflation Rates in History?

Hungary holds the record for history’s worst inflation from 1945-1946, when prices doubled every 15.6 hours and reached 13.6 quadrillion percent.

A loaf of bread jumped from 6 pengő to 6 billion pengő in just one year.

More recently, Zimbabwe hit 79.6 billion percent inflation, while Venezuela reached about 9,586 percent.

These extreme cases show how wars and poor economic policies can destroy currencies.

How Does Inflation Affect My Purchasing Power and Savings?

Inflation gradually chips away at purchasing power by making everything more expensive while paychecks often stay the same.

If groceries cost $100 today but inflation runs at 3%, those same items will cost $103 next year.

Meanwhile, savings sitting in low-interest accounts lose value over time. A dollar today buys less tomorrow, which explains why grandparents often say things were cheaper back in their day.